What’s in store in 2024?

As we wind down for holiday season, it’s a great moment to look ahead and plan for potential opportunities.

Biotech finance has been sparce in 2022 and 2023, especially in Europe, and companies who have run low on financing during this period have had a rough ride. Indeed, some have been left no choice but to shut down or accept similarly unattractive alternatives.

Geopolitical uncertainty, higher inflation and interest rates have underpinned volatility in global markets over the last two years, leading spooked investors to avoid risky investments, like pre-revenue biotechnology companies. But this has arguably only compounded the real issue, which is the hangover that has followed the exuberant outpouring of financial resources into biotech during the Covid-19 pandemic. And the hangover comes in various shapes and forms, from outflows from earlier stage companies to a diffuse demand that both biotech and also commercial-stage medtech adjust their expense bases in a new, deflationary environment, to preserve the cash raised over the 2019-21 period.

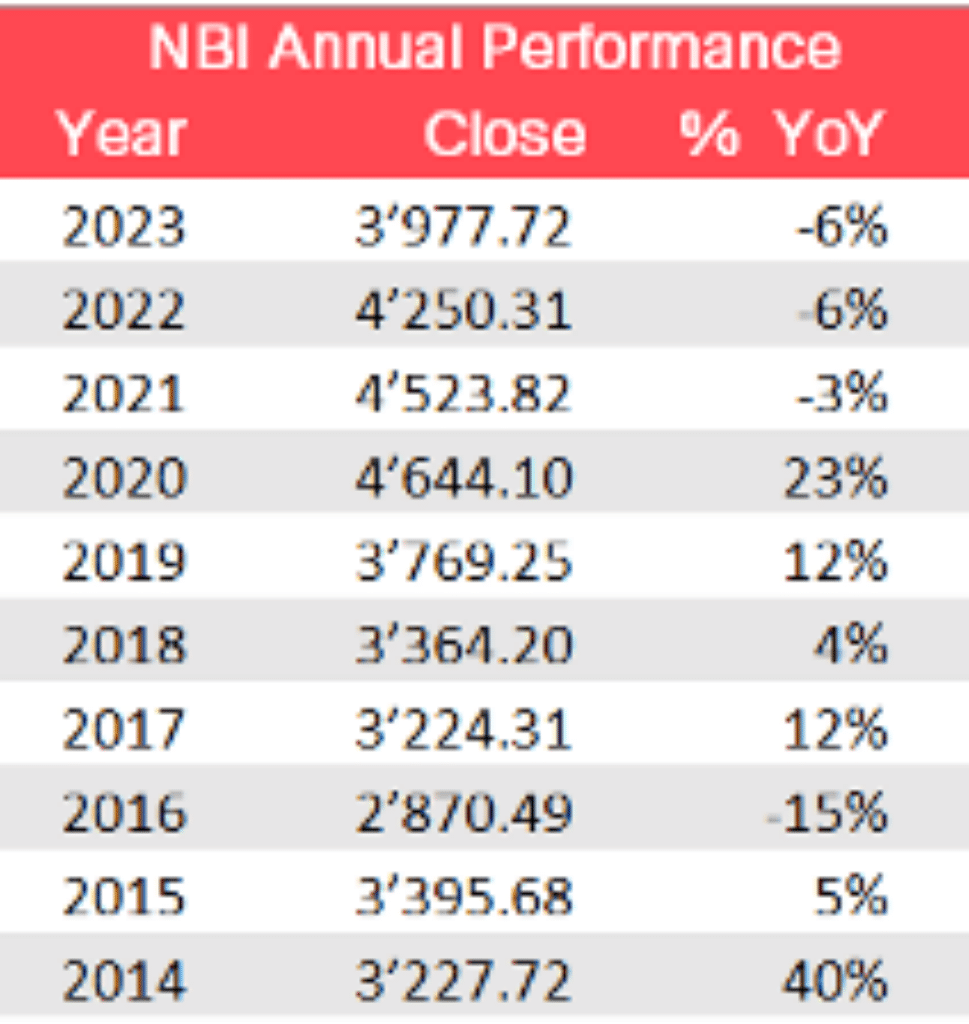

A jaw-dropping 128 biotech companies went public in the U.S. in 2021 and 99 in 2020. Not all of these initial public offerings (IPOs) were on Nasdaq, but even so, the Nasdaq Biotechnology Index (NBI; first launched on 1 November 1993) roughly doubled to 371 constituents over 2020 and 2021. During the eight years prior to 2020 – most of which were considered “good” years for biotech financing (at least in the U.S.) – the NBI constituents increased by an average of about 12 companies per year.

So, it’s no wonder that the industry is experiencing some indigestion after the incredible financing smorgasbord served up by Covid-19.

Positive signs

There are signs that the symptoms brought on by this excess are resolving, and already, there are encouraging indications that next year may be better. This is supported by emerging data, our anecdotal discussions and, of course, the continuing acceleration of progress and innovation in important areas of medical need. On December 6, 2023, Nasdaq listed European biopharma Pharvaris raised $300 million the same day it announced impressive Phase 2 data for deucrictibant, its oral bradykinin B2 receptor antagonist, in the prevention of HAD attacks. That revealed investors’ readiness, perhaps even impatience, to support clinical success in already relatively crowded indications and substantial valuations.

For example, the UK biotech sector raised £563 million in venture capital and public financings in Q3 2023, data from Biotech Finance show, making it the strongest period since the historical highs of 2021. One of the largest private biotech rounds in Europe this year was completed in November, with VectorY Therapeutics’ €129 million Series A financing. There was another glimmer of hope early in Q4 2023 when Paris-based inflammatory disease company Abivax completed a USD 236 million Nasdaq IPO.

And then there’s Big Pharma, with plenty of cash burning holes in its pockets from blockbuster sales of treatments for diseases like Covid-19, metabolic disorders and cancer. But even when times are good for Big Pharma, their awesome marketing capabilities cannot stop their products’ patent clocks, and they must continue to fill their pipelines.

Big Pharma spending

At recent industry conferences, Big Pharma told us that they think that rights to most late-stage biotech assets have either been acquired or are over-priced. Thus, they have turned their attention to acquiring earlier stage assets, specifically products between preclinical and clinical proof of concept.

And, indeed, there were 83 M&A deals announced In the European pharmaceutical industry in Q3 2023, worth a total $10.7 billion – more than doubling from Q3 2022 –, according to GlobalData, with the largest disclosed deal being the $5.7 billion acquisition of Abcam by Danaher. More recently, Boehringer Ingelheim has announced the acquisition of privately-held Swiss biotech T3 Pharmaceuticals for CHF 450 million. The joint acquisitions of early-stage Lyon, France-based Mablink Bioscience and its PSARlink ADC platform and of its licensee for Nectin-4 target Emergence Therapeutics, for undisclosed amounts, are strong examples of earlier stage acquisition by Big Pharma enriched by obesity drug success, in this case tirzepatide.

In January 2024, the industry will gather around the JP Morgan Healthcare Conference in San Francisco, and we expect this partnering trend to be the talk of the town.

It goes without saying that the prospect of Big Pharma spending excites biotech investors, inviting speculation on which companies might be the most attractive. This could drive increased investment in venture stage and small-cap public biotech in 2024.